I spent years in fintech before I understood what adjusted gross income actually meant. Not the textbook definition — I could recite that. But what it actually controls, and why it matters more than almost any other number on your tax return.

When I started Jupid, my first full year of US self-employment income was a crash course in how AGI works. I earned money from the business. I contributed to a SEP-IRA. I paid self-employment tax. I paid for my own health insurance. Each of those actions affected my AGI, and my AGI in turn determined whether I qualified for the QBI deduction, how much I could contribute to a Roth IRA, and what tax credits were available to me.

At Anna Money in the UK, where we served 60,000+ small businesses, we saw a similar dynamic with the Personal Allowance — the UK equivalent of certain income-based thresholds. Once your income exceeds a certain level, you start losing tax benefits. The US version of this mechanism runs through AGI.

For self-employed people, AGI is the most important number on your tax return. It's not your gross income — it's your gross income after specific "above-the-line" deductions that only self-employed people and business owners get access to. Lower your AGI and you may qualify for deductions and credits that save you thousands. Ignore it and you'll pay more tax than you need to.

This guide walks through exactly what AGI is, how to calculate it, which deductions reduce it, and why it matters so much for self-employed filers in 2026.

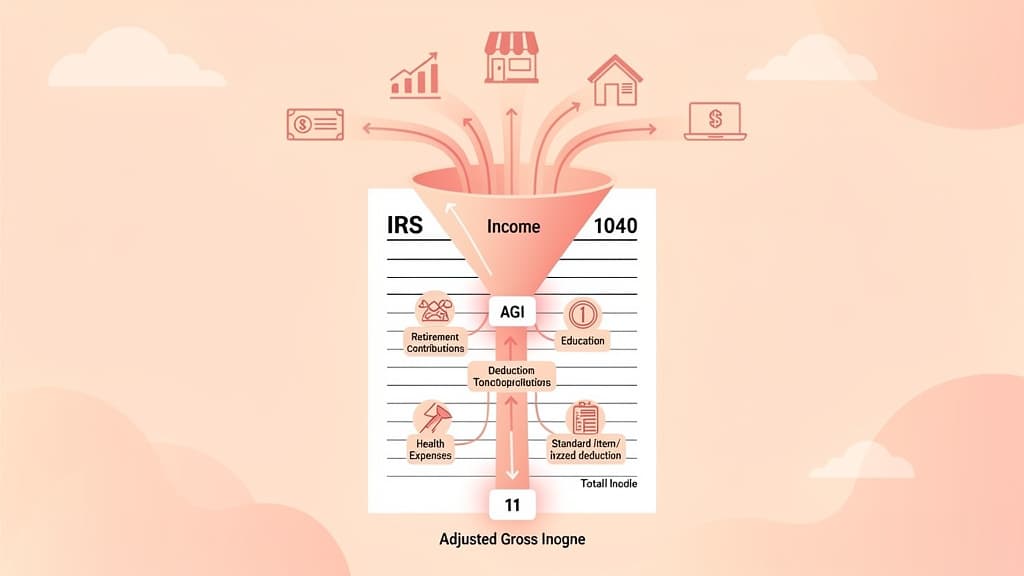

What is AGI? Your total income from all sources minus specific "above-the-line" deductions. Found on Form 1040, Line 11.

2026 AGI Overview:

Factor

Details

Where to find AGI

Form 1040, Line 11

Total income

All wages, business income, investments, retirement distributions, etc.

Above-the-line deductions

Half of SE tax, SE health insurance, IRA contributions, HSA, student loan interest

Why AGI matters

Determines eligibility for QBI deduction, Roth IRA, EITC, premium tax credit, education credits, and more

MAGI vs. AGI

MAGI = AGI + certain items added back (varies by provision)

SE tax deduction

Deduct 50% of self-employment tax above the line

SE health insurance

100% deductible above the line (if not eligible for employer plan)

IRA contribution limit

$7,500 ($8,600 if age 50+)

HSA contribution limit

$4,400 (self-only) / $8,750 (family)

Student loan interest

Up to $2,500

Key point: AGI is calculated before you take the standard deduction or itemize. Every dollar that reduces your AGI can have a cascading effect — reducing your taxable income and potentially qualifying you for additional deductions and credits.

Legal basis: IRC Section 62 (definition of adjusted gross income), IRS Form 1040, IRS Publication 17

Adjusted gross income is your total income from all sources, minus a specific set of deductions called "above-the-line" deductions or "adjustments to income."

The term "above the line" refers to the line on Form 1040 where AGI appears (Line 11). Deductions taken above this line reduce your AGI directly. Deductions taken below the line (the standard deduction or itemized deductions) reduce your taxable income but do not affect your AGI.

Your total income includes everything reported on Form 1040, Lines 1 through 9:

Income Source

Form 1040 Line

Common for Self-Employed?

Wages, salaries, tips

Line 1a

If you have a day job

Tax-exempt interest

Line 2a

Sometimes

Taxable interest

Line 2b

Yes (business bank accounts)

Ordinary dividends

Line 3a

If you have investments

Qualified dividends

Line 3b

If you have investments

IRA distributions

Line 4a-4b

If you took distributions

Pensions and annuities

Line 5a-5b

Less common

Social Security benefits

Line 6a-6b

If applicable

Net business income (Schedule C)

Line 8

Yes — this is the big one

Capital gains/losses

Line 7

If you sold assets

Other income (Schedule 1)

Line 8

Rental income, K-1 income, etc.

For self-employed people, the largest component is typically Line 8: net business income from Schedule C. This is your business revenue minus your business expenses.

Your Schedule C profit flows directly into your Form 1040 and becomes part of your total income. This is where accurate expense tracking matters enormously.

Example: Schedule C for a freelance consultant

Item

Amount

Gross revenue

$120,000

Business expenses (office, software, travel, supplies, etc.)

-$25,000

Home office deduction

-$5,000

Net Schedule C income

$90,000

That $90,000 flows to Form 1040 as part of your total income. Every legitimate business expense you claim on Schedule C reduces this number — and by extension, reduces your AGI.

Jordan's total income is $110,500, but after above-the-line deductions, the AGI drops to $72,585. This lower AGI determines Jordan's eligibility for the QBI deduction, Roth IRA contributions, and various credits.

Self-employed individuals pay both the employer and employee portions of Social Security and Medicare taxes — a combined 15.3% on net self-employment earnings (12.4% Social Security on earnings up to $176,100, plus 2.9% Medicare on all earnings).

The IRS allows you to deduct the employer-equivalent portion (half) as an above-the-line adjustment. This deduction is automatic — you don't need to itemize to claim it.

Calculation for 2026:

Net SE income x 92.35% = SE tax base

SE tax base x 15.3% = total SE tax

Total SE tax x 50% = above-the-line deduction

Example: $100,000 net SE income x 0.9235 = $92,350 x 0.153 = $14,130 total SE tax. Deduction = $7,065.

If you're self-employed and not eligible for a subsidized health plan through an employer (yours or a spouse's), you can deduct 100% of your health insurance premiums above the line. This includes:

Medical, dental, and vision insurance for you, your spouse, and dependents

Long-term care insurance premiums (age-based limits apply)

Premiums for your children under age 27, even if they're not dependents

The deduction is limited to your net self-employment income. You cannot use it to create a business loss.

Contributions to certain retirement plans are deductible above the line:

SEP-IRA: Up to 25% of net self-employment earnings (after the SE tax deduction), maximum $70,000 for 2026. This is the most common retirement plan for sole proprietors because it's simple to set up and allows large contributions.

Solo 401(k): Employee contributions up to $24,500 ($32,500 if age 50+), plus employer contributions of up to 25% of net SE earnings. Combined maximum of $70,000 ($77,500 if age 50+).

SIMPLE IRA: Employee contributions up to $16,500 ($20,000 if age 50+), plus employer match.

Traditional IRA: Up to $7,500 ($8,600 if age 50+). Deductibility may be limited if you or your spouse is covered by an employer retirement plan and your MAGI exceeds certain thresholds.

Health Savings Account contributions are deductible above the line if you have a qualifying High Deductible Health Plan (HDHP).

2026 HSA limits:

Self-only coverage: $4,400

Family coverage: $8,750

Additional catch-up (age 55+): $1,000

Starting in 2026, bronze and catastrophic plans available through a Health Insurance Exchange are considered HSA-compatible regardless of whether they meet the traditional HDHP definition — expanding eligibility significantly.

You can deduct up to $2,500 in student loan interest paid during the year. This deduction phases out for 2026 when MAGI is between $85,000 and $100,000 (single) or $175,000 and $205,000 (married filing jointly).

This deduction is available even if you don't itemize — it's an above-the-line adjustment.

The 20% QBI deduction allows eligible self-employed filers to deduct up to 20% of their qualified business income. But eligibility and limitations are based on your taxable income, which is directly derived from your AGI.

For 2026, if your taxable income exceeds $197,300 (single) or $394,600 (MFJ), limitations based on W-2 wages paid and qualified property begin to apply. If you're in a "specified service trade or business" (consulting, law, accounting, health, etc.), the deduction phases out entirely above those thresholds.

Lower AGI = lower taxable income = full QBI deduction.

Your ability to contribute to a Roth IRA depends on your MAGI (which starts with AGI):

Filing Status

Full Contribution

Phase-Out

No Contribution

Single/HOH

MAGI under $153,000

$153,000-$168,000

Over $168,000

MFJ

MAGI under $242,000

$242,000-$252,000

Over $252,000

If your AGI is close to these thresholds, above-the-line deductions like SEP-IRA contributions or HSA contributions could bring your MAGI below the limit and allow full Roth IRA contributions.

If you buy health insurance through the ACA marketplace, the premium tax credit is based on your household income relative to the Federal Poverty Level. Household income uses MAGI. Lower AGI means higher subsidies and lower insurance costs.

Self-employed filers with net SE income can qualify for the EITC if their AGI falls below certain thresholds. For 2026, the maximum credit for a taxpayer with three or more children is approximately $7,830. AGI limits vary by filing status and number of children.

The American Opportunity Tax Credit and Lifetime Learning Credit both phase out based on MAGI. Lower AGI preserves access to up to $2,500 per student (AOTC) or $2,000 per return (LLC).

Medical expenses are deductible only to the extent they exceed 7.5% of your AGI. Lower AGI means a lower threshold, which means more of your medical expenses are deductible.

Modified Adjusted Gross Income (MAGI) starts with your AGI and adds back certain deductions. The exact add-backs depend on which tax provision you're calculating MAGI for.

Traditional IRA deduction, student loan interest deduction, foreign earned income exclusion

Premium tax credit

Tax-exempt interest, non-taxable Social Security benefits

Student loan interest deduction

Student loan interest deduction itself (circular — uses AGI for this one)

Medicare premium surcharges (IRMAA)

Tax-exempt interest, foreign earned income exclusion

Child tax credit

Generally the same as AGI

SALT cap phaseout

Specific MAGI definition under OBBBA

For most self-employed filers, MAGI and AGI are very close or identical. The add-backs are typically small unless you have foreign earned income, tax-exempt interest, or student loan interest.

Understanding the path from business revenue to AGI is critical for self-employed filers:

Business Revenue (Schedule C, Line 1)

- Cost of Goods Sold (Line 4)

= Gross Profit (Line 7)

- Business Expenses (Lines 8-27)

= Net Business Income (Schedule C, Line 31)

↓

Form 1040, Schedule 1, Line 3

↓

Form 1040, Line 8 (Total Income component)

↓

Minus Above-the-Line Deductions (Schedule 1, Part II)

↓

Form 1040, Line 11 = AGI

Every step in this chain matters:

Maximize legitimate Schedule C deductions — Every business expense reduces net income. See our business expense categories guide for a complete list.

Claim above-the-line deductions — Half of SE tax, health insurance, retirement contributions, HSA. These reduce AGI beyond what Schedule C alone achieves.

The cascading effect — Lower Schedule C income means lower SE tax, which means a higher half-of-SE-tax deduction, which further reduces AGI. The benefits compound.

A SEP-IRA contribution of up to $70,000 is the single most powerful AGI-reduction tool for high-earning self-employed filers. If your net SE earnings support it, this one move can drop your AGI by tens of thousands of dollars.

Example: Net SE earnings of $200,000 → SEP-IRA contribution of $50,000 → AGI reduced by $50,000.

The $4,400 (self-only) or $8,750 (family) HSA contribution is an above-the-line deduction that also grows tax-free and can be withdrawn tax-free for medical expenses. It's the only account with a triple tax benefit.

Starting in 2026, if you're enrolled in a bronze or catastrophic plan through the Exchange, you're now HSA-eligible even if the plan doesn't meet traditional HDHP definitions.

If you're paying for your own health insurance, deducting premiums above the line reduces your AGI dollar for dollar. Don't forget dental and vision premiums — they qualify too.

Business expenses reduce Schedule C income, which reduces AGI. The difference between careful expense tracking and rough estimates can be thousands of dollars. Common missed deductions include:

AGI is not your taxable income. Taxable income is AGI minus the standard deduction (or itemized deductions) and the QBI deduction. Many self-employed filers look at their AGI and panic, not realizing their taxable income is significantly lower after these additional deductions.

A freelancer earning $160,000 might assume they can contribute to a Roth IRA. But if their MAGI (starting from AGI) is over $168,000, they can't contribute at all. Understanding the connection between AGI and eligibility thresholds is essential for tax planning.

Self-employed health insurance premiums are deducted on Schedule 1 (above the line), not on Schedule C. Putting them on Schedule C reduces your net SE income, which reduces your SE tax — but also reduces your QBI and your half-of-SE-tax deduction. The IRS requires the deduction on Schedule 1, and placing it there produces the correct result.

The IRS uses your prior year AGI as an identity verification when you e-file. If you enter the wrong amount, your return will be rejected. Keep a copy of your prior year return or use the IRS transcript tool to look it up before filing.

Your AGI starts with your Schedule C income — which means accurate expense tracking is the foundation of AGI management. Jupid connects to your bank accounts and categorizes every transaction with 95.9% accuracy using IRS Schedule C categories.

Here's how Jupid helps you manage your AGI:

Automatic expense categorization — Every deductible business expense is identified and categorized, reducing your Schedule C income and by extension your AGI. No manual spreadsheet work required.

Real-time income tracking — Jupid separates business income from personal deposits, giving you an accurate picture of your net SE income throughout the year — not just at tax time

Self-employment tax calculations — Jupid calculates your SE tax based on actual income, which determines both your tax liability and your above-the-line deduction for half of SE tax

Tax liability estimates — See your estimated federal and state tax bills based on current income and expenses, so you can make informed decisions about retirement contributions, timing, and quarterly payments

AI accountant via WhatsApp and iMessage — Ask questions like "What's my estimated AGI for 2026?" or "How much can I contribute to a SEP-IRA?" and get answers based on your actual financial data

For self-employed filers, every dollar of AGI reduction can unlock additional savings through the QBI deduction, Roth IRA eligibility, and premium tax credits. The first step is knowing your numbers accurately.

AGI is the single most consequential number on your tax return as a self-employed person. It determines your tax bracket, your eligibility for deductions and credits, and your access to retirement savings vehicles. Track your income and expenses accurately throughout the year, claim every above-the-line deduction you qualify for, and make retirement and HSA contributions strategically.

Disclaimer:This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently, and individual circumstances vary. Consult a qualified tax professional for advice specific to your situation. Jupid provides AI-powered transaction categorization and tax estimates but is not a substitute for professional tax counsel.

Fintech CEO with 10+ years building accounting and financial technology products. Previously co-founded and scaled an AI-powered accounting platform to $30M revenue and 100K+ business users, achieving 30,000 customers per accountant through automation — recognized by CNBC as a top fintech company. Holds a Master's in Management Information Systems. At Jupid, he leads the development of AI-native bookkeeping, tax, and compliance tools designed for freelancers and small business owners.