The IRS selects returns for audit mostly by computer score, not at random. A Discriminant Function (DIF) score flags returns whose deductions fall outside the statistical norm for a taxpayer's income and industry, and an automated information-matching system catches income that doesn't match the 1099s and W-2s already on file. Overall audit rates are low, roughly 0.4% of individual returns in recent IRS Data Book years, but specific Schedule C patterns raise a self-employed filer's odds. The documented triggers below are the ones you control.

Key takeaways:

- Every return gets a DIF (Discriminant Function) score, plus a separate UI-DIF score for suspected unreported income

- Automated information matching (your 1099s and W-2s against your return) catches mismatches before any human review, and it is the most common trigger

- Documented Schedule C red flags: high deductions relative to income, repeated losses (the §183 hobby-loss rule), 100% business vehicle use, round numbers, and unreported cash

- The overall individual audit rate is about 0.4% (IRS Data Book); the IRS has said new enforcement is aimed at incomes over $400,000, not under

- Statute of limitations: 3 years standard, 6 years if you understate income by 25%+, and unlimited if you never file or commit fraud

What is an IRS audit? A formal examination of your tax return to verify that your reported income, deductions, and credits are accurate.

2026 Audit Overview:

| Factor | Details |

|---|

| Overall audit rate | ~0.4% of individual returns (recent IRS Data Book) |

| Self-employed audit rate | Higher than average due to Schedule C complexity |

| $1M+ income audit rate | Around 1% and up, rising with each income tier (IRS Data Book) |

| Highest-income audit rate | Among the highest tiers; the IRS has set multi-year targets to raise audits on the wealthiest and on large partnerships |

| Selection method | DIF scoring system + information matching |

| Statute of limitations | 3 years (standard), 6 years (25%+ understatement), unlimited (fraud/no return) |

| Types of audits | Correspondence, office, field |

Key point: The IRS has committed to not increasing audit rates for individuals earning under $400,000 per year. But self-employed filers at any income level can trigger an audit through specific return characteristics.

Legal basis: IRC §7602 (audit authority), IRC §6501 (statute of limitations), IRS Publication 556 (Examination of Returns)

The IRS doesn't review every return manually. Instead, it uses a computerized system called the Discriminant Function System (DIF) to score every return based on the likelihood of errors or underreported income.

Your DIF score is a numerical rating assigned to your tax return. The IRS compares your return to statistical norms for taxpayers with similar:

- Income levels

- Filing status

- Industry (NAICS code)

- Geographic location

- Deduction patterns

Returns that deviate significantly from these norms receive higher DIF scores. The higher your score, the more likely your return will be selected for review.

- Every return gets scored. The DIF system assigns a composite score based on weighted factors.

- High-scoring returns are flagged. The returns that deviate most from the statistical norm are routed for possible examination.

- Human review follows. An IRS examiner, not the computer, decides which flagged returns become actual audits, so a high DIF score does not automatically mean an audit.

- The formulas are secret. The IRS has never publicly disclosed the exact DIF formulas. They are classified as confidential and for official use only.

What this means for you: If your deductions are proportionally much higher or lower than other people in your industry and income range, your DIF score goes up. The goal isn't to claim fewer deductions — it's to claim accurate deductions with documentation to back them up.

In addition to the standard DIF, the IRS uses a separate Unreported Income DIF (UI-DIF) score. This one specifically flags returns where the IRS suspects income may be underreported. It's particularly relevant for:

- Cash-heavy businesses (restaurants, salons, contractors)

- Businesses with significant cost-of-goods-sold discrepancies

- Returns where third-party information (1099s, bank deposits) doesn't match reported income

This is the number one trigger for self-employed audits. If your total business expense deductions consume a disproportionately large percentage of your gross income, your return stands out statistically.

Example: A freelance consultant reports $80,000 in gross income and $72,000 in deductions, leaving only $8,000 in net profit. The IRS compares this to other consultants earning $80,000, most of whom report $20,000–$40,000 in deductions. The high deduction-to-income ratio raises the DIF score.

What to do: Claim every deduction you're entitled to — but make sure each one is legitimate, documented, and directly related to your business. The IRS doesn't penalize high deductions when they're substantiated. They penalize patterns that suggest inflated or fabricated expenses.

Reporting a loss on your Schedule C isn't illegal — but it's a red flag, especially if it happens multiple years in a row.

Under IRC §183 (the "hobby loss" rule), the IRS can reclassify your business as a hobby if it doesn't show a profit in at least 3 out of 5 consecutive years. Hobby expenses are not deductible against other income.

Trigger intensity: A single year of losses is common for new businesses. Three or more consecutive years of losses, particularly when the taxpayer has other income sources, will almost certainly increase your DIF score.

If you operate in an industry where cash transactions are common (restaurants, bars, hair salons, car washes, construction, lawn care), the IRS pays closer attention. Cash income is harder to trace through third-party reporting, making underreporting more likely.

The IRS has industry-specific benchmarks for cash-intensive businesses. If your reported income falls below what they'd expect based on your industry and location, expect scrutiny.

The home office deduction is legitimate and valuable, but it's also one of the most commonly inflated deductions. The IRS knows this and scrutinizes large home office claims, especially when:

- The deducted square footage seems high relative to the home's total size

- The taxpayer also rents a separate office space

- The claimed expenses (utilities, repairs, insurance) are disproportionate

For 2026: The simplified method allows $5 per square foot, up to 300 square feet ($1,500 maximum). The actual expense method (Form 8829) can yield higher deductions but requires precise documentation.

This one is surprisingly effective as a trigger. When every line on your Schedule C ends in zeros ($5,000 for supplies, $3,000 for travel, $2,000 for meals), it signals estimation rather than actual record-keeping.

Real business expenses rarely come out to round numbers. A $4,847.32 deduction looks like it came from actual receipts. A $5,000 deduction looks like a guess.

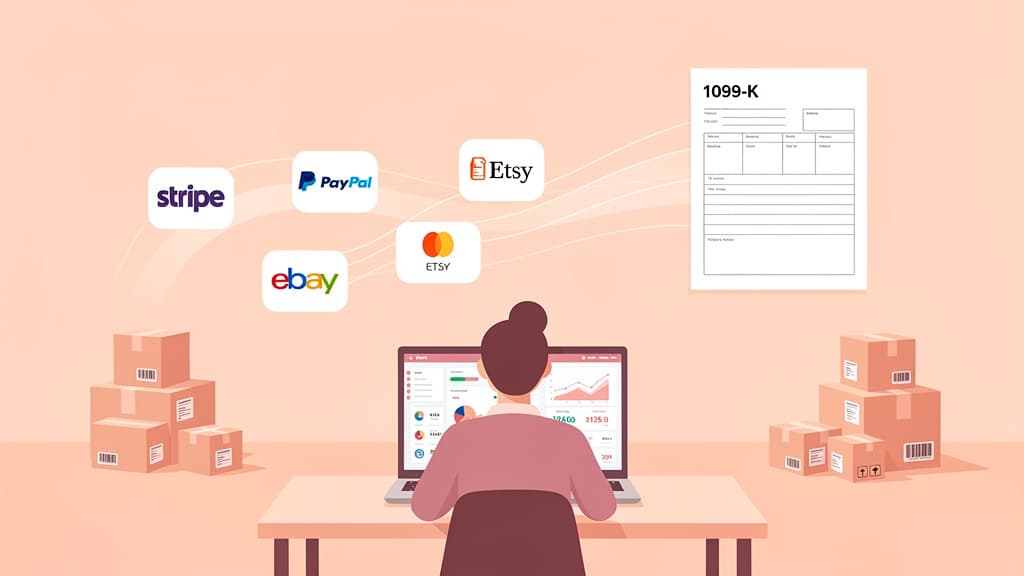

The IRS receives copies of every 1099 issued to you. Starting in 2026, the 1099-NEC reporting threshold has increased from $600 to $2,000, but you're still required to report all self-employment income, including amounts below the threshold.

If the total income on your Schedule C doesn't match or exceed the total of all 1099s the IRS has on file, the mismatch triggers an automatic notice, often before any DIF analysis even occurs.

Charitable deductions that significantly exceed the norm for your income level raise flags. If you earn $75,000 and claim $20,000 in charitable contributions, the IRS will want to see documentation.

For non-cash contributions exceeding $500, you must file Form 8283. For donations exceeding $5,000, you'll generally need a qualified appraisal.

Not filing a return doesn't prevent an audit — it invites one. The IRS tracks who should be filing based on W-2s, 1099s, and other information returns. If they have records showing you earned income but you didn't file, they'll eventually come looking.

If you haven't filed, see our guide on what happens if you don't file taxes.

Claiming 100% business use of a vehicle is a significant red flag unless you have a dedicated business vehicle that is never used personally. Most taxpayers use their vehicle for both business and personal purposes, and the IRS knows this.

For 2026: The standard mileage rate is 72.5 cents per mile. If you claim the actual expense method, you must maintain a contemporaneous mileage log that separates business from personal use.

If your Schedule C income fluctuates dramatically year over year without a clear explanation (for example, $150,000 one year and $40,000 the next), the IRS may flag the lower year for examination. Similarly, claiming a deduction type one year but not others (such as a large equipment purchase with no related income increase) can trigger questions.

Not all taxpayers face the same audit risk. Based on recent IRS Data Book figures, audit rates break down roughly as follows. These rates shift year to year and stay historically low for most filers:

| Income Level | Approximate Audit Rate |

|---|

| Under $25,000 (no total positive income) | ~0.3% (about 3 per 1,000) |

| $1 – $24,999 | ~0.4% (about 4 per 1,000) |

| $25,000 – $49,999 | ~0.2% (about 2 per 1,000) |

| $50,000 – $499,999 | ~0.1% (about 1 per 1,000) |

| $500,000 – $999,999 | ~1% |

| $1,000,000 – $4,999,999 | ~1% (about 11 per 1,000) |

| $5,000,000 – $9,999,999 | A few percent |

| $10,000,000+ | The highest tier, several percent in recent years and rising under IRS targets |

Why are low-income returns audited? The Earned Income Tax Credit (EITC) drives audit activity at the lower end. EITC claimants face audit rates of 0.7–1.5%, higher than many middle-income taxpayers.

The IRS enforcement focus for 2026: The IRS has stated it will concentrate new enforcement resources on taxpayers earning over $400,000, large partnerships, and corporations. If you're a small business owner earning under $400,000, your audit rate should remain stable — but only if your return doesn't contain the red flags listed above.

The most common type, accounting for about 75% of all audits. The IRS sends you a letter asking for documentation to support specific items on your return — a particular deduction, a credit, or an income discrepancy.

What to expect: You mail or fax the requested documents. If the IRS accepts your documentation, the audit closes. If they don't, they'll propose adjustments and give you 30 days to agree or appeal.

Common targets: EITC claims, itemized deductions, specific Schedule C line items.

The IRS asks you to bring documents to a local IRS office for an in-person review. These are more thorough than correspondence audits and typically cover multiple issues on your return.

What to expect: You'll receive a letter specifying which items are being examined and what documentation to bring. You can bring a representative (CPA, enrolled agent, or attorney) with you, or send them in your place with a power of attorney (Form 2848).

The most thorough type. An IRS revenue agent visits your home or business to examine your records in detail. Field audits typically target higher-income taxpayers, businesses, and complex returns.

What to expect: The agent may review bank statements, contracts, invoices, receipts, and business records for multiple years. Field audits can take weeks or months to complete and often cover more ground than the initial notification suggests.

The IRS sends a letter (never a phone call or email — that's a scam) identifying:

- Which tax year(s) are being examined

- Which specific items are under review

- What documentation you need to provide

- Your deadline to respond (usually 30 days)

You provide the requested documentation. For self-employed filers, this typically includes:

- Bank statements showing business income deposits

- Receipts and invoices supporting deductions

- Mileage logs for vehicle deductions

- Home office measurements and expense records

- Contracts with clients

After reviewing your documents, the IRS either:

- Accepts your return as filed (no changes)

- Proposes adjustments (additional tax, penalties, or interest owed)

- Issues a refund (if the audit reveals you overpaid — this does happen)

If the IRS proposes adjustments you disagree with, you can:

- Request a meeting with the examiner's manager

- File an appeal with the IRS Office of Appeals

- Take it to Tax Court (you must petition within 90 days of receiving a Notice of Deficiency)

Legal citation: IRC §7602 grants the IRS authority to examine books, records, and witnesses. IRS Publication 556 outlines the examination process.

The IRS doesn't have unlimited time to audit you. The statute of limitations sets time limits on how far back they can go:

| Situation | Time Limit |

|---|

| Standard | 3 years from filing date (or due date, whichever is later) |

| 25%+ income understatement | 6 years |

| Fraud | No limit |

| No return filed | No limit |

| Amended return | 3 years from the amended return filing date (for new items) |

What "25% understatement" means: If you omitted more than 25% of your gross income from your return, the IRS gets 6 years instead of 3. This applies to both understated income and overstated basis in property sales.

Filing gives you protection. Once you file a return, the 3-year clock starts. If you never file, there's no statute of limitations — the IRS can come after you at any time.

Legal citation: IRC §6501 governs the statute of limitations on assessments.

This is the single most effective audit defense. For every deduction you claim on Schedule C:

- Save the receipt or invoice

- Note the business purpose

- Record the date and amount

- Keep records for at least 3 years (7 years is safer)

The $2,000 1099-NEC reporting threshold for 2026 doesn't change your obligation to report every dollar of self-employment income. Report it all on Schedule C, even if you don't receive a 1099.

Review your records and enter precise amounts. $4,847.32 is more credible than $5,000. If you're estimating because you don't have records, that's a sign your record-keeping needs improvement.

Open a dedicated business bank account. Use a separate credit card for business purchases. When business and personal expenses are commingled, it's harder to prove which expenses are deductible — and the IRS may disallow all of them.

If you claim vehicle expenses, keep a contemporaneous log (written at the time of the trip, not reconstructed later) that records:

- Date of each trip

- Starting and ending locations

- Business purpose

- Miles driven

If you claim the actual expense method for your home office deduction, measure and document:

- Total square footage of your home

- Square footage of your dedicated office space

- The percentage of home expenses allocated to business use

Filing late or not filing at all draws attention. If you need more time, file an extension (Form 4868) — but remember, an extension to file is not an extension to pay. You still need to pay estimated taxes by the original deadline.

If your income and deductions swing wildly from year to year, include documentation or notes that explain why. Starting a new business, making a large equipment purchase, or losing a major client are all legitimate reasons for fluctuations, but the IRS doesn't know your story unless you can tell it.

Mistake #1: Claiming personal expenses as business deductions. Your Netflix subscription, personal gym membership, and daily coffee aren't business expenses. The IRS has seen every creative justification and they don't buy them.

Mistake #2: Not reporting income because you didn't get a 1099. The $2,000 threshold means your payer doesn't have to file a 1099 — but you still owe tax on the income. The IRS cross-references bank deposits and payment processor data. They will find the discrepancy.

Mistake #3: Using round numbers for every deduction. This signals estimation instead of actual record-keeping. Real expenses have cents. Report the actual amounts.

Mistake #4: Claiming 100% business use of a vehicle you also drive personally. Unless you have a separate vehicle used exclusively for business, the IRS will question this. Most agents know that 100% business use is extremely rare for sole proprietors.

Mistake #5: Panicking and ignoring an audit notice. Ignoring an IRS letter doesn't make it go away — it makes it worse. The IRS will proceed without your input and assess the maximum tax, plus penalties and interest. Always respond by the deadline.

The best audit defense is good record-keeping, and that's exactly what Jupid is built for. Instead of scrambling to find receipts and reconstruct records when an audit notice arrives, Jupid keeps your finances organized automatically, all year long.

Automatic transaction categorization. Jupid connects to your bank accounts and categorizes your business transactions with 95.9% accuracy. Every expense is sorted into the correct Schedule C category, with no manual data entry, no guessing, and no round numbers.

Real-time expense tracking. Every transaction is recorded as it happens, creating the contemporaneous records the IRS looks for. When your deductions are backed by actual bank data with precise amounts and dates, there's nothing to question.

AI-powered tax guidance via WhatsApp and iMessage. Not sure if an expense is deductible? Ask Jupid's AI accountant directly from your phone. Get answers based on current IRS rules, not generic advice from a search engine. This helps you make the right call in the moment, before tax season arrives.

Separation of business and personal. Jupid tracks your business transactions separately, making it simple to prove which expenses are business-related. No more commingling nightmares.

Year-round readiness. Because Jupid categorizes and tracks throughout the year, your records are always audit-ready. If a letter arrives, you have organized, accurate documentation from day one.

Start building your audit-proof records today at Jupid.

IRS audits are not random. They follow patterns, and those patterns are knowable. Keep accurate records, report all your income, use precise numbers instead of estimates, and separate business from personal expenses. Do those four things consistently and your audit risk drops to near zero.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax laws change frequently. Consult a qualified tax professional for advice specific to your situation. Jupid provides automated bookkeeping and tax categorization — we are not a CPA firm or tax advisory service.